The latest Bureau of Economic Analysis (BEA) data gave us a mixed read on consumer prices for September.

Energy, food, and goods prices dropped, nudging headline inflation closer to the Fed’s 2% target. But services inflation is still sticky high, suggesting the Fed may lean toward keeping rates elevated for longer rather than rushing to ease up.

The Core PCE price index—one of the Fed’s key inflation gauges—rose 0.3% for the month, right in line with expectations and a slight uptick from August’s revised 0.2%. Year-over-year, core PCE remained steady at 2.7%, still above that 2% target.

For the broader PCE, which includes those more volatile food and energy costs, we saw a consistent 0.2% monthly increase. However, the yearly rate edged down just a touch from 2.2% to 2.1%.

On the income and spending front, personal income picked up slightly, rising from 0.2% to 0.3% as expected, while spending surged from 0.3% to 0.5%.

Adding to this, the dip in the personal savings rate—now at 4.6%, down from 5.2% in June—and spending gains across areas like healthcare, housing, and durable goods hint at resilient consumer activity amidst moderating inflation and high interest rates.

Link to U.S. Personal Income and Outlays Report for September 2024

In a separate release, the Labor Department reported 216,000 initial jobless claimants in the week ending October 26, fewer than the previous week’s 228,000 claimants and the expected 229,000 figure.

Link to Department of Labor’s weekly initial jobless claims report

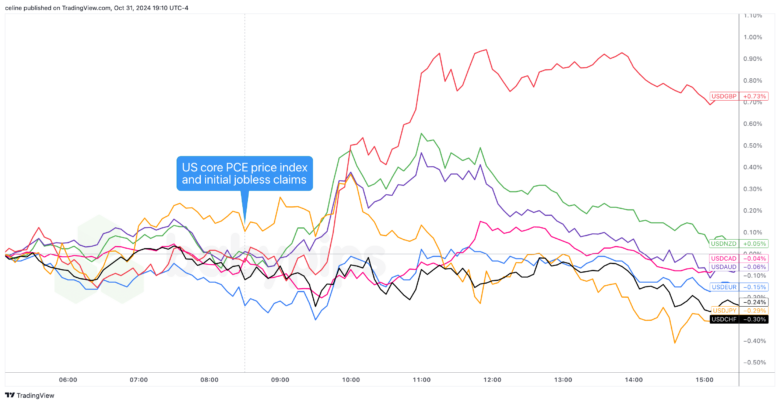

U.S. dollar vs. Major Currencies: 5-min

Overlay of USD vs. Major Currencies Charts by TradingView

The U.S. dollar started turning lower about an hour before the core PCE price index report and saw limited initial reaction to the release.

However, the evidence of moderating inflation, strong consumer prospects, and better-than-expected weekly initial jobless claims data soon supported USD demand.

The Greenback swung higher against “riskier” currencies like AUD, NZD, EUR, and GBP before pulling back down and ending the day in ranges above its U.S. session lows.