The Bank of Canada (BOC) held its policy rate at 2.75% in April, its first pause after seven consecutive rate cuts since June 2024.

This decision came amid extreme uncertainty about U.S. trade policies, with Governor Tiff Macklem stating, “We still do not know what tariffs will be imposed, whether they’ll be reduced or escalated, or how long all of this will last.”

Key Points from BOC’s Event

- BOC held the overnight rate at 2.75%

- Trade uncertainty made it “impossible to issue regular economic forecasts”

- Presented two scenarios instead of a central forecast

- Economy entered 2025 with solid Q4/2024 growth of 2.6%

- First quarter 2025 GDP growth estimated at 1.8%, slower than expected

- Employment declined in March, with businesses reporting plans to slow hiring

- Removal of consumer carbon tax expected to pull down inflation to 1.5% in April

- “Monetary policy cannot resolve trade uncertainty or offset the impacts of a trade war”

Link to official BOC April monetary policy statement

In his press conference, Governor Macklem emphasized that monetary policy would “proceed carefully” with particular attention to risks, being “less forward-looking than usual” until the trade situation clarifies, while standing ready to “act decisively” if evidence points clearly in one direction.

He explained that the current policy sits at the midpoint of the neutral rate range (2.25-3.25%) and warned that, in a severe scenario, the consequences would be “painful” for Canada. Specifically, some exporters could go bankrupt, unemployment could rise, and Canadians might need to cut back spending.

Senior Deputy Governor Carolyn Rogers later revealed there were differing opinions among Governing Council members about the potential economic impact of U.S. tariffs, with some officials being “more optimistic that the effects won’t be really big.”

Link to BOC April monetary policy press conference

In a separate release, BOC’s April Monetary Policy Report scrapped its traditional economic forecasts for the first time since the COVID-19 pandemic, instead presenting two illustrative scenarios due to extreme uncertainty around U.S. trade policies.

The first scenario assumes most tariffs are eventually negotiated away, resulting in temporarily stalled GDP growth followed by moderate expansion, with inflation dropping below the 2% target before returning to it.

The second, more severe scenario depicts a protracted global trade war causing a year-long recession in Canada with GDP contracting for four quarters, permanently reducing Canada’s potential output and temporarily pushing inflation above 3% by mid-2026 before returning to target in 2027.

Link to BOC April Monetary Policy Report

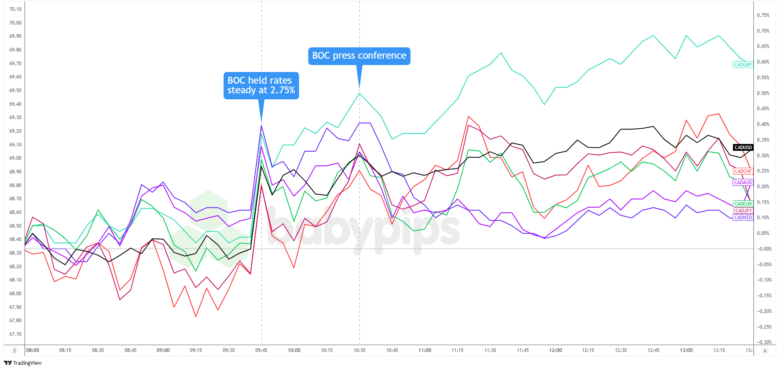

Market Reactions

Canadian Dollar vs. Major Currencies: 5-min

Overlay of CAD vs. Major Currencies Chart by TradingView

The Canadian dollar, which chopped around in the early U.S. session, surged after BOC paused its interest rate cuts. Traders took the Bank’s tone as relatively less dovish, especially given Wednesday’s uncertain backdrop.

But the Loonie quickly pulled back down as traders digested the uncertainty around the Bank’s response to tariff scenarios.

Later, Macklem’s steady tone and the Bank’s readiness to “act decisively” likely gave CAD a boost, but the currency eventually chopped around some more as the markets responded to risk sentiment-related headlines. CAD ended the day mixed, closing higher against USD and “risk” currencies like AUD, NZD, and GBP but losing ground against the other majors.

Markets are now split on the June decision, pricing in about a 50% chance of a cut and roughly 50 basis points of easing by year-end.